A structural shift in the global vegetable oil market—characterized by the decoupling of palm oil’s growth momentum from the acreage expansion of ‘soft oils’ (soybean, rapeseed, and sunflower)—is fundamentally reshaping the demand patterns, seasonal volatility, and geographic centers of gravity within the global fertilizer market.

The global vegetable oil market is undergoing a profound structural shift, with palm oil’s growth engine stalling while “soft oils” like soybean, sunflower, and rapeseed expand to fill the void. This transition is not merely a commodity rebalancing; it is a fundamental reconfiguration of the global fertilizer market.

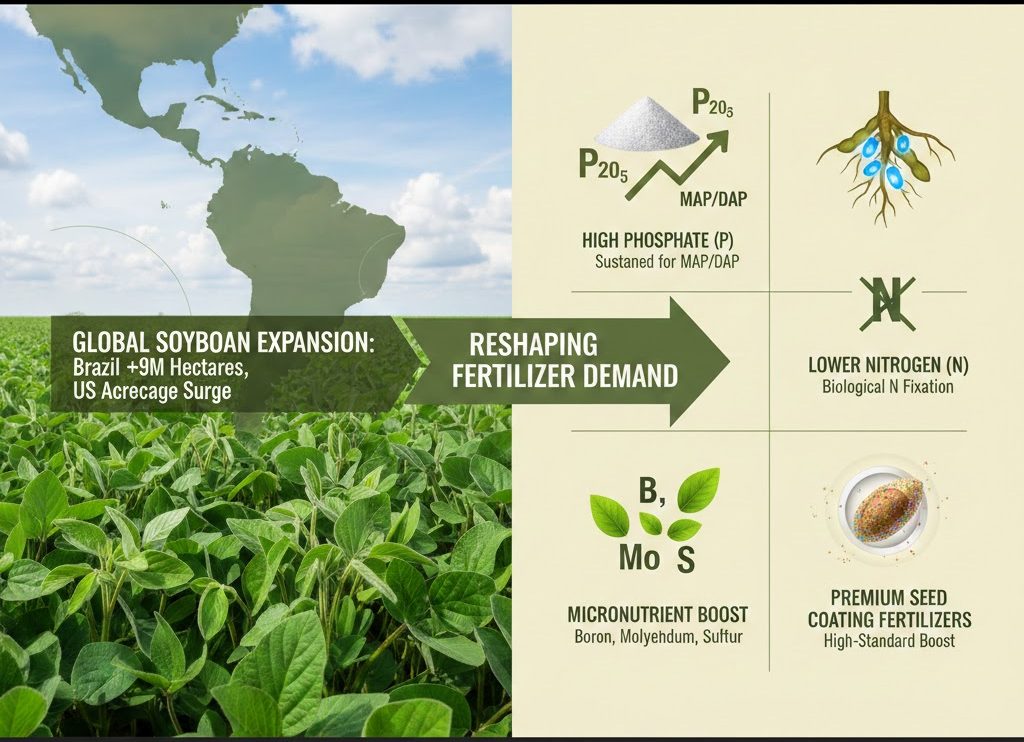

1. Structural Growth in Global Fertilizer Demand

The transition from high-yield perennial crops (oil palm) to lower-yield annual crops (soybeans, etc.) is a primary driver of increased nutrient consumption.

-

Yield-to-Efficiency Ratio: Oil palm yields approximately 3.5–4.0 tons of oil per hectare, whereas soybeans yield only 0.4–0.6 tons. To compensate for a projected 6-million-ton shortfall in palm oil exports, tens of millions of additional hectares of soft oils must be cultivated.

-

The “Leverage Effect” on Total Volume: While oil palm is a nutrient-intensive crop, its exceptional land-use efficiency means the fertilizer required per ton of oil produced is relatively low. As the global production center shifts toward soft oils, total global fertilizer consumption is set to enter an upward trajectory driven by massive acreage expansion.

2. Shift in Nutrient Preferences and Product Mix

Variations in the nutritional requirements of different crops are causing a divergence in fertilizer demand:

-

Potash (MOP) Pressure in Palm Regions: Potassium is the critical nutrient for oil palm. However, large-scale plantation seizures in Indonesia and management neglect due to aging plantations in Malaysia are expected to suppress the import premium for MOP in Southeast Asia in the short term.

-

Phosphate (MAP/DAP) and Specialty Fertilizers in Soybean Hubs: Rapid acreage expansion in Brazil and the U.S. will sustain high demand for phosphates. Furthermore, since soybeans are nitrogen-fixing, the market will see a shift away from urea toward secondary and micronutrients (Boron, Molybdenum, Sulfur) and high-standard seed-coating fertilizers.

3. Geographical Realignment of Trade Flows

-

Eastern Hemisphere (Southeast Asia): A Shift toward “Quality”: The palm oil sector is moving from horizontal expansion to vertical productivity gains via “high-yield seeds” and “automation.” Consequently, the Southeast Asian market will transition from bulk commodities toward high-efficiency compound fertilizers and water-soluble fertilizers tailored for precision agriculture.

-

Western Hemisphere (Americas): A Shift toward “Quantity”: The Americas will act as the primary engine for acreage expansion. Global fertilizer trade flows will increasingly concentrate toward key logistics hubs such as the Port of Santos and New Orleans.

4. Heightened Sensitivity to Seasonal Volatility and Price Linkage

-

Price Transmission Mechanism: With palm oil prices projected to rise to $1,000–$1,350 per ton in 2026, improved farm income will enhance farmers’ tolerance for higher input costs, supporting fertilizer price levels.

-

Risk Factors: Supply uncertainties in Indonesia and Malaysia may trigger “panic planting” in South America. If Indonesian yields drop sharply in Q3 2026, it could lead to impulse demand spikes for fertilizers, significantly increasing price volatility in the global spot market.

5. Regulatory Influence of Biofuel Policies

-

Biofuel Mandates (B40/B50) and EPA Rulings: If the U.S. EPA confirms robust biomass-based diesel mandates in March 2026, the resulting surge in soybean oil prices will immediately trigger advance fertilizer orders in the U.S. Midwest. Fertilizer suppliers must monitor these policy milestones as they are the primary determinants of restocking intensity for the spring application season.